UPDATED 12 April: The Senate Banking Committee held a stacked hearing on "Assessing Consumer Regulations" yesterday (5 April), although our one pro-consumer witness and pro-CFPB Senators defended consumer protection ably as three industry-backed witnesses and their supporters on the committee had a great deal of trouble proving their case that the CFPB should be dismantled. Tomorrow morning, (7 April) CFPB Director Richard Cordray will present the statutory "Semi-Annual Report of the CFPB" to the committee. We submitted a statement to be entered into the hearing record, as did other Americans for Financial Reform coalition members.

UPDATED 12 April: I stand corrected. CFPB Director Richard Cordray’s appearance (written statement) last Thursday was the Bureau’s 61st (not mere 59th) testimony before Congress. Also, ranking member Sherrod Brown (OH) has posted a release “ICYMI: Public Interest Advocates Praise CFPB’s Success in Protecting Consumers” which excerpts from and links to each of 12 statements for the record from Americans for Financial Reform and its member groups, including ours. The hearing went well as the director explained the various enforcement,

educational, rulemaking and other successes that the bureau has had had in just four-and-one-half years.

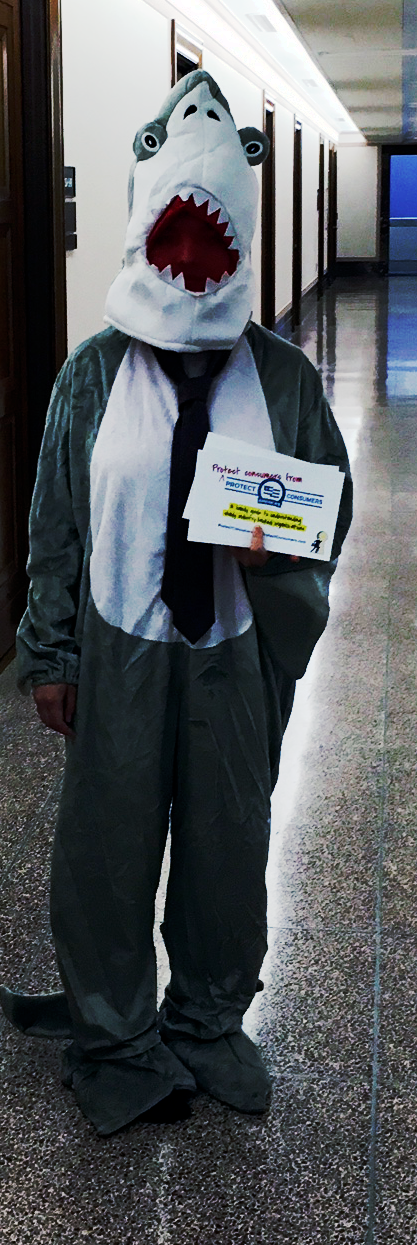

Notably, a number of citizen CFPB supporters, dressed in CFPB green T-shirts emblazoned “Stand up for the CFPB,” attended the hearing. I had a CFPB green tie, so we all contrasted with the phalanx of paid lobbyists forced to sit behind us (we got there early). A “payday loan shark” also attended to promote the welcome new protectconsumersfromprotectconsumers.com web site, which targets one of the deceptive, dark-money (no disclosure), astroturf (no grassroots) anti-CFPB sites I had mentioned below.

ORIGINAL POST: While the House Financial Services Committee has held numerous hearings and voted out numerous bills attacking the Consumer Financial Protection Bureau (CFPB) and consumer protection generally in this Congress, the Senate Banking Committee had largely been on hiatus for months while its chairman Richard Shelby (AL) campaigned to win his March primary. Now, he’s back, and aiming his sights at the CFPB, too.

The Senate Banking Committee held a stacked hearing on “Assessing Consumer Regulations” yesterday (April 4) and will hear the “Semi-Annual Report of the Consumer Financial Protection Bureau (CFPB)” tomorrow morning (April 6). (Hearings are live on video; post-hearing video archives and written testimony of in-person witnesses are available at those links.) We submitted a statement to be entered into the hearing records, as did other Americans for Financial Reform (AFR) coalition members.

Yesterday, although the hearing witnesses were stacked 3-1 against the CFPB, our one pro-consumer witness, the Reverend Willie Gable, and pro-CFPB Senators led by Elizabeth Warren (MA), ranking member Sherrod Brown (OH) and Jeff Merkley (OR) defended consumer protection ably. Meanwhile, three industry-backed witnesses and their supporters on the committee had a great deal of trouble proving their case that the CFPB or any consumer regulations should be dismantled.

In an electrifying exchange, Senator Warren (Youtube video) challenged an industry lawyer’s views and suitability as a witness because he’d been a longtime Federal Reserve official both before and during the Fed’s failure to identify or respond to many warnings of market conditions and mortgage industry practices that led to the 2008 financial meltdown and subsequent recession.

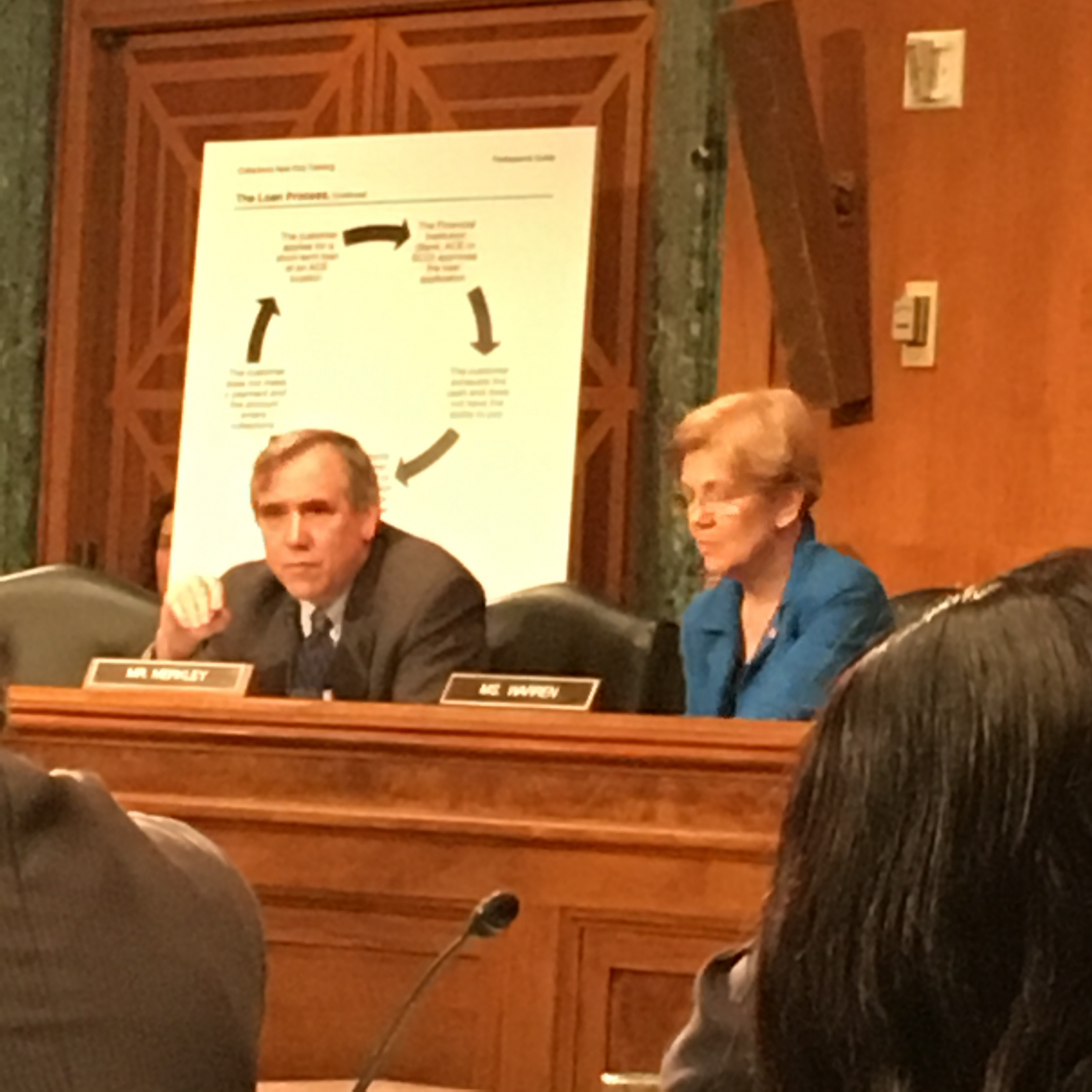

Senator Merkley emphasized the problems with the payday loan business model, which creates an unsustainable “cycle of debt” as his chart at right shows.

Our new blog “What Is Payday Lending?” has more. Payday lenders are among the shrillest opponents of the CFPB, and are seeking to kill its proposed regulation to regulate predatory high-cost short-term lending. Their campaign goes so far as to run ads in my own personal Facebook feed and probably in yours. too. CFPB opponents including the payday lenders, credit bureaus, the American Bankers Association, the Consumer Bankers Association and U.S. Chamber of Commerce (which also had a witness yesterday) are also joined by a number of dark-money (no disclosure) fake consumer groups running Astroturf (no grassroots) campaigns on the Internet.

For his part, Senator Brown engaged hostile witnesses on a variety of subjects, including defense of the CFPB’s Public Consumer Complaint Database, which was also the core subject of our statement to the committee (see below). He also explained the history of the financial collapse, and warned the committee not to engage in “collective amnesia” by repealing the protections enacted to prevent a repeat of the 2008 collapse.

A frequent critique of the CFPB is that it lacks oversight. Tomorrow morning, CFPB Director Richard Cordray will present the statutory “Semi-Annual Report of the CFPB” to the committee. The notion that the CFPB lacks oversight or is out-of-control is rebutted by the simple fact that Director Cordray’s appearance tomorrow will be approximately the 59th testimony by him or other senior bureau officials before Congress since the agency was “stood up” on July 21, 2011 as the nation’s first regulator with just one job, protecting consumers.

He has presented the report already in the House, so it is available (most recent, Fall 2015, is subject of these hearings). It is a formidable and encyclopedic report (summary of most recent report in Director Cordray’s House testimony in March) yet it is by no means the only oversight document of the CFPB. For example, here are a few other recent oversight documents:

Our statement for the record focuses on three issues (with excerpts below):

Our full statement to be entered into the hearing records explains each of these points in much greater detail.

Conversely, Senator Shelby’s opening remarks simply repeated many old themes of House attacks on the CFPB. So did questions from other Senators from his party. The notion that we don’t need a consumer regulator or consumer regulations is also rebutted, of course, by the Senator Warren Youtube excerpt from yesterday.

We agree with detailed comments of over a dozen statements submitted for the record from other Americans for Financial Reform (AFR) coalition members. Each of our AFR statements provides detail on 1-2 important consumer regulations, from credit reporting to mortgage regulations; all statements also point out, in their own words, that “the idea of the CFPB needs no defense, only more defenders.”

Senior Director, Federal Consumer Program, PIRG

Ed oversees U.S. PIRG’s federal consumer program, helping to lead national efforts to improve consumer credit reporting laws, identity theft protections, product safety regulations and more. Ed is co-founder and continuing leader of the coalition, Americans For Financial Reform, which fought for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, including as its centerpiece the Consumer Financial Protection Bureau. He was awarded the Consumer Federation of America's Esther Peterson Consumer Service Award in 2006, Privacy International's Brandeis Award in 2003, and numerous annual "Top Lobbyist" awards from The Hill and other outlets. Ed lives in Virginia, and on weekends he enjoys biking with friends on the many local bicycle trails.